The Fragility of the Last Mile: A Policy Analysis of Independent Community Pharmacies, PBM Vertical Integration, and the Preservation of Public Health Equity – RESEARCH & PODCAST SERIES 2026

Structural Misalignment in U.S. Drug Pricing

A Policy Framework for Federal and State Regulators Addressing the Collapse of Independent Pharmacy Infrastructure.

I. Ecosystem Consolidation

Pharmacy Benefit Managers (PBMs) operate as oligopolistic intermediaries, capturing margins through spread pricing and vertical integration with insurers. This structural misalignment drains capital from frontline providers.

II. The Reimbursement Crisis

A massive 107,400% increase in DIR fees (retroactive clawbacks) since 2010 has inverted pharmacy operating margins.

Underwater MAC pricing forces pharmacies to lose capital on essential generic therapeutics.

Contract Inelasticity

Pharmacies cannot negotiate terms; refusal leads to immediate network exclusion and loss of patient access.

III. Public Health Consequence

Closure of independent pharmacies triggers catastrophic drops in medication adherence, creating “Pharmacy Deserts.”

Adherence Drop

Decrease in chronic medication adherence following a local pharmacy closure.

Access Risk

Multiplier of risk for non-English speaking and rural populations.

IV. Operational Excellence

Independent models provide clinical services that corporate volume-driven models cannot economically sustain.

- • Multilingual Care: Cultural bridging in immigrant corridors.

- • Complex Packaging: Supporting disability centers like Harbor House.

- • MTM Services: Direct clinical counseling and therapy management.

V. Policy Recommendations

Federal

Mandate floor reimbursement at NADAC + Dispensing Fee; Ban spread pricing in Part D.

State

Strengthen MAC appeal enforcement via DOI; Enforce Rutledge v. PCMA protections.

Reform

Shift from product-based to service-based payment (clinical CPT codes).

The Institutional Decline of the Community Pharmacy in the Twenty-First Century

The American pharmaceutical distribution chain, once a decentralized network of community-based health hubs, has undergone a radical structural transformation over the last two decades. At the heart of this shift is the independent community pharmacy, an institution that serves as the primary point of clinical contact for millions of Americans, particularly those in rural, low-income, and medically underserved areas. However, the economic viability of these pharmacies is currently under unprecedented threat due to a convergence of market consolidation, predatory reimbursement models, and complex regulatory gaps. As the intermediaries known as Pharmacy Benefit Managers (PBMs) have evolved from administrative claims processors into vertically integrated behemoths, the independent pharmacy has been forced into a role where it often loses money on the very life-saving medications it dispenses.1

The contemporary state of independent pharmacy is defined by a paradox of essentiality and fragility. While these pharmacies provide a range of critical benefits—including timely medical guidance, screening services, and enhanced medication management that lead to better health outcomes—they are simultaneously being squeezed out of existence by the firms that control their reimbursement.2 The Federal Trade Commission (FTC) has characterized the current environment as one where PBMs "dominate" independent pharmacies, exercising significant power over Americans' access to drugs and the prices consumers pay.1 This dominance is not merely a byproduct of market efficiency but is the result of intentional vertical integration that aligns health plans, PBMs, and pharmacy assets under single corporate umbrellas, creating incentives to prefer affiliated businesses to the detriment of unaffiliated competitors.1

Market Concentration and the Rise of the Vertical Monolith

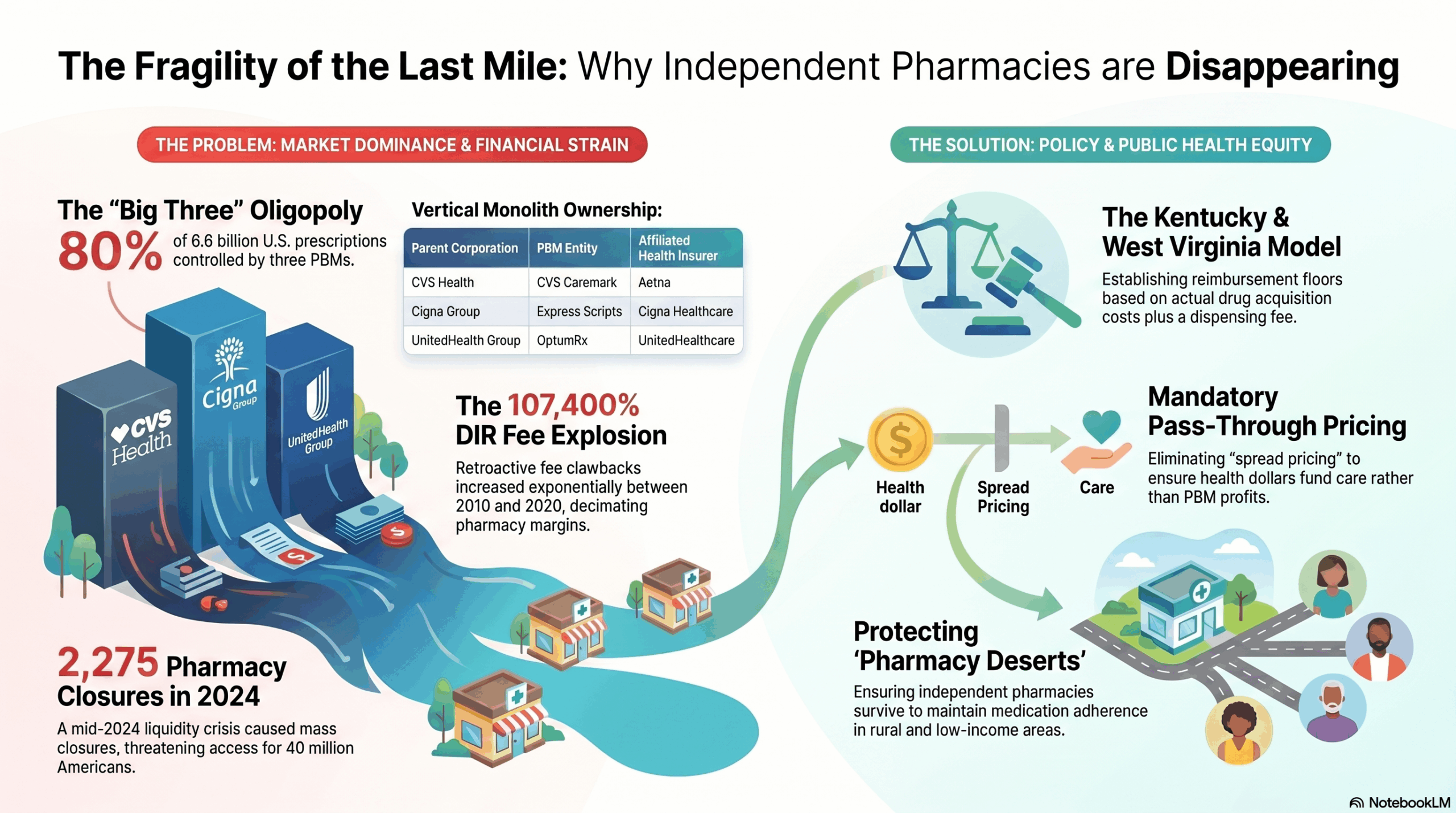

The pharmaceutical supply chain is currently governed by a state of extreme oligopoly. The structural evolution of the PBM industry from service-based administrators to dominant market gatekeepers has fundamentally altered the competitive landscape. As of 2024, the "Big Three" PBMs—CVS Caremark, Express Scripts, and OptumRx—manage nearly 80% of the approximately 6.6 billion prescriptions dispensed in the United States.1 When extending the analysis to the top six PBMs, the market share exceeds 90%, leaving independent pharmacies with virtually no bargaining power.4

This concentration is further complicated by vertical integration, where the largest PBMs are owned by or affiliated with the nation’s largest health insurers and specialty pharmacies. This alignment creates a closed-loop system that can effectively exclude independent pharmacies from participation in lucrative networks or specialty drug dispensing.

The Landscape of Vertical Integration

| PBM Entity | Parent Corporation | Affiliated Health Insurer | Affiliated Pharmacy Assets |

| CVS Caremark | CVS Health | Aetna | CVS Pharmacy, CVS Specialty |

| Express Scripts (ESI) | Cigna Group | Cigna Healthcare | Accredo (Specialty), Express Scripts Pharmacy |

| OptumRx | UnitedHealth Group | UnitedHealthcare | Optum Specialty Pharmacy |

| Humana Pharmacy Solutions | Humana | Humana | CenterWell Pharmacy |

| Prime Therapeutics | 19 Blue Cross Blue Shield Plans | Various BCBS Plans | AllianceRx (Specialty) |

1

The implications of this integration are profound. Vertically integrated PBMs have both the ability and the incentive to "self-preference" their own affiliated businesses. This manifests through the steering of patients toward PBM-owned mail-order or retail pharmacies, often through the use of "preferred network" designs that impose higher cost-sharing on patients who choose to use their local independent pharmacist.1 In the specialty drug sector, this steering has been particularly effective; pharmacies affiliated with the Big Three PBMs received 68% of the dispensing revenue generated by specialty drugs in 2023, a significant increase from 54% in 2016.8

Furthermore, the FTC’s 2024 interim report highlights that these integrated entities often negotiate "complex and opaque" contractual relationships that disadvantage smaller, unaffiliated pharmacies.1 These contracts frequently include below-cost reimbursement rates and arbitrary fees that make it impossible for independent pharmacies to remain financially viable. The FTC notes that for certain specialty generic drugs, affiliated pharmacies are sometimes paid 20 to 40 times the National Average Drug Acquisition Cost (NADAC), while unaffiliated pharmacies receive significantly less.4

The Financial Mechanics of Pharmacy Attrition: DIR Fees and the 2024 Crisis

The most destructive financial pressure facing independent pharmacies over the last decade has been the exponential growth of Direct and Indirect Remuneration (DIR) fees. Originally conceived under the Medicare Part D program as a mechanism to account for manufacturer rebates and pharmacy performance adjustments, DIR fees were repurposed by PBMs as retroactive clawbacks. These fees are assessed weeks or months after a prescription has been filled, meaning that a pharmacy may not know its actual reimbursement for a drug until long after the transaction has concluded.9

The DIR Fee Explosion (2010–2020)

Between 2010 and 2020, CMS reported that retroactive DIR fees increased by a staggering 107,400%.9 By 2023, these assessments had grown from less than 0.5% of total prescription sales in 2015 to 3.7%.3 This growth reflects a shift in the PBM business model away from transparent administrative fees toward a "punitive and complex matrix" of risk models that decimate pharmacy profit margins.3

The impact of these fees is not limited to the pharmacy’s balance sheet; they also result in higher costs for patients. Because the "negotiated price" at the pharmacy counter often did not include these retroactive fees, patients’ coinsurance—which is typically a percentage of the negotiated price—was calculated on an artificially inflated base.9

The 2024 "DIR Hangover" and the Liquidity Gap

In response to advocacy from the pharmacy community, CMS issued a final rule that eliminated the retroactive application of DIR fees starting January 1, 2024. The rule required that all pharmacy price concessions be reflected in the negotiated price at the point of sale.9 While intended to provide transparency and predictability, the implementation of this rule triggered a severe liquidity crisis known as the "DIR apocalypse" or "DIR hangover".3

Independent pharmacies faced a "one-two punch" in early 2024. They were required to accept lower point-of-sale reimbursements (reflecting the upfront 2024 fees) while simultaneously paying off the retroactive DIR fees incurred during the final months of 2023.3 This simultaneous obligation "strangled" cash flow, with some pharmacy owners reporting debts of $100,000 or more as a direct result of the rule change.3 The transition period proved fatal for many; by September 16, 2024, approximately 2,275 pharmacies had closed their doors for the year.3

| Impact Category | Pre-2024 Model | 2024 Reform Model | Resulting Financial Stress |

| Fee Timing | Retroactive (months later) | Upfront (at point of sale) | "Double-dip" payment period in early 2024 |

| Transparency | Low (reimbursement uncertain) | High (lowest possible reimbursement visible) | Revealed that many prescriptions are filled at a loss |

| Patient Cost | Higher (based on gross price) | Lower (based on net price) | Plans may reduce reimbursement further to offset loss |

| Cash Flow | Predictable but deferred | Immediate but lower | Sudden drain on liquidity for small businesses |

3

The Opaque Economy of Rebates and Spread Pricing

Central to the PBM profit model is the negotiation of prescription drug rebates from manufacturers. PBMs argue that these rebates are used to lower premiums for plan sponsors. However, the FTC and other regulators have raised concerns that the rebate system creates "perverse" incentives that favor high-priced drugs over more affordable alternatives.1

The FTC's 2024 lawsuit against the Big Three PBMs specifically targets their role in inflating the list price of insulin. The complaint alleges that PBMs prioritized "high price, highly rebated" insulins on their flagship formularies, effectively excluding lower-priced versions even when they became available.5 By basing their own fees and compensation on a drug's list price, PBMs benefit from price increases, a dynamic that "flipped healthy price competition on its head".5

Spread Pricing and Generic Effective Rates (GER)

In addition to rebates, PBMs utilize "spread pricing," where they charge a health plan more for a drug than they reimburse the pharmacy. While some states have moved to ban this practice in Medicaid programs, it remains prevalent in the commercial sector.11 To further control reimbursement, PBMs use Generic Effective Rates (GER) and Brand Effective Rates (BER), which allow them to aggregate pharmacy performance and claw back payments across entire drug categories to meet pre-negotiated targets. For independent pharmacies, these rates are often set at "untenably low levels," forcing them to operate at a loss on many common medications.2

Independent Pharmacies as Essential Infrastructure for Underserved Populations

The decline of independent pharmacies is a crisis of public health equity. Independent pharmacies are disproportionately likely to be located in rural areas and low-income urban neighborhoods—communities that are often "pharmacy deserts".13 When a local pharmacy closes, the distance between patients and their medication increases, which has been shown to worsen health outcomes and increase mortality rates.14

Pharmacy Deserts and Medication Adherence

Over 40 million Americans currently reside in pharmacy deserts.14 Research published in JAMA Network Open has established a statistically significant association between pharmacy closures and decreased medication adherence among adults 50 years and older.15 For chronic conditions requiring statins, β-blockers, and oral anticoagulants, the closure of a local pharmacy often leads to patients rationing their doses or going without medication entirely.14

Conversely, the presence of an independent pharmacy can be a primary facilitator of adherence. Independent pharmacists often provide "enhanced services" that large chains and mail-order providers do not, such as home delivery, multidose compliance packaging, and personalized adherence coaching.16

Specialized Care for Vulnerable Populations: Case Studies

The role of the independent pharmacist as a clinical advocate is best illustrated through specialized care models. One notable example is the Kentucky Pharmacy at the Harbor House of Louisville. Harbor House is a facility dedicated to supporting adults with developmental and physical disabilities.17

| Service Feature | Implementation at Kentucky Pharmacy | Impact on Underserved Population |

| Physical Integration | Located inside a $17M disability care facility | Provides immediate, secure access for patients with mobility issues |

| Multilingual Support | CEO Dr. Vy Truong and staff offer diverse language services | Bridges care gaps for immigrants and refugees with limited English |

| Direct Advocacy | Making physician calls for patients fearful of the system | Ensures patients receive appropriate therapies despite cultural barriers |

| Personalized Delivery | Hand-delivering prescriptions to the homebound in all weather | Prevents medication lapses for the elderly and those without transport |

19

In another case, the North Carolina Community Pharmacy Enhanced Services Network (CPESN) has demonstrated the clinical value of integrating pharmacists into the "medical home" team. A study of NC-CPESN pharmacies found that patients using these "enhanced services" pharmacies had persistently higher adherence scores for Medicaid-covered medications, with differences ranging from 3.0% to 7.2% compared to control pharmacies.13 These improved outcomes are directly attributed to the provision of multidose compliance packaging and delivery services.13

The Jurisdictional Shift: State-Level Policy Interventions

As federal action remained slow for decades, states emerged as the primary laboratories for PBM regulation. The legal foundation for this shift was solidified by the 2020 Supreme Court ruling in Rutledge v. PCMA.

Rutledge v. PCMA and the Erosion of ERISA Preemption

In Rutledge, the Supreme Court held that an Arkansas law regulating PBM reimbursement rates was not preempted by the Employee Retirement Income Security Act (ERISA).21 The Court clarified that ERISA does not prevent states from implementing "cost regulations" that affect the finances of ERISA plans but do not dictate the plans' core administrative structures.22 This landmark decision opened the door for states to enact laws protecting independent pharmacies from below-cost reimbursement.

Kentucky’s Regulatory Model: A Case Study in Medicaid Reform

Kentucky has been a national leader in PBM reform, primarily through Senate Bill 50 (2020) and Senate Bill 188 (2024). Senate Bill 50 required the state Department for Medicaid Services to establish a single, state-administered PBM for the entire Medicaid program, effectively ending the practice of spread pricing and opaque rebating within Managed Care Organizations (MCOs).11

The methodology for assessing the success of SB 50 involved analyzing Managed Care Pharmacy costs before and after implementation:

.24

The transition to a single PBM (MedImpact) and a single Preferred Drug List (PDL) resulted in an 8.6% reduction in per-member per-month (PMPM) costs in 2021 as rebates were maximized and passed back to the state.24 Without SB 50, it is estimated that total pharmacy expenditures in Kentucky would have been $172.5 million higher in 2021 and $110.2 million higher in 2022.24

Building on this, SB 188 (2024) extended protections to the commercial market, establishing a reimbursement floor for independent pharmacies based on the National Average Drug Acquisition Cost (NADAC) plus a professional dispensing fee of $10.64.25 This bill also prohibits retroactive fees and limits the ability of PBMs to force patients toward PBM-owned specialty or mail-order pharmacies.25

West Virginia and the Push for Transparency

West Virginia enacted Senate Bill 453 in 2024, which focuses on the Public Employees Insurance Agency (PEIA). The law creates a reimbursement floor for pharmacies at NADAC plus a $10.49 professional dispensing fee, specifically aimed at stabilizing the state's independent pharmacy infrastructure.25 The bill also mandates monthly reporting from PBMs to ensure transparency in how much is charged to the state versus how much is paid to providers.27

The Inflation Reduction Act: New Challenges for Small Business Viability

While state reforms provide a defensive shield, federal policy changes under the Inflation Reduction Act (IRA) of 2022 introduce new systemic risks. The IRA’s Medicare Drug Price Negotiation Program (MDPNP) aims to lower costs for seniors, but its operational implementation may inadvertently harm small pharmacies.28

Maximum Fair Price (MFP) and Cash Flow Shortfalls

Starting in 2026, the first ten negotiated drugs will be available at their Maximum Fair Price (MFP). However, the "effectuation" of these prices is complex. Pharmacies will be required to dispense these drugs at the lower MFP, but they face potential delays in being reimbursed for the difference between their acquisition cost and the MFP.28

Analysis from 3 Axis Advisors suggests that pharmacies could lose nearly $11,000 in weekly cash flow due to payment settlement delays for negotiated drugs.28 Over a year, an average independent pharmacy could forfeit $43,000 in revenue—a figure roughly equivalent to the salary of a pharmacy technician.28 Without "adequate protection" to absorb these changes, the IRA could trigger a secondary wave of pharmacy closures, leaving seniors without a local provider to dispense the very drugs the law aimed to make affordable.28

The Part D Redesign and Premium Stabilization

The IRA also redesigns the Part D benefit, implementing a $2,000 out-of-pocket cap for beneficiaries starting in 2025.30 This shift significantly increases the liability of Part D plans for drug spending.31 To mitigate massive premium increases, CMS implemented a Premium Stabilization Demonstration for 2025, providing insurers with $15 per month per enrollee to offset costs.30 However, the long-term sustainability of this model remains uncertain, and plans may respond to their increased liability by further squeezing pharmacy reimbursement rates or tightening network adequacy standards.

Antitrust and the Future of Regulatory Enforcement

The legal battle against PBM practices is increasingly moving into the realm of antitrust. Critics argue that the vertical integration of PBMs facilitates anti-competitive conduct that violates the Sherman Act.6

Monopolization and Exclusionary Conduct

Under Section 2 of the Sherman Act, PBMs are accused of using their market power to maintain dominance in specialty drug markets. In recent litigation, plaintiffs have alleged that PBMs were bribed or incentivized by brand manufacturers to direct patients away from lower-cost generics.33 Furthermore, the FTC is exploring whether PBMs are violating the FTC Act’s Section 5, which prohibits "unfair methods of competition".5

The FTC’s current leadership, influenced by "Neo-Brandeisian" philosophy, argues that antitrust enforcement must look beyond immediate consumer prices to the structural health of the market.6 From this perspective, the "destruction" of independent pharmacies by chain-owned PBMs is an injury to competition that warrants aggressive intervention, including the potential for structural separation—forcing corporations to divest either their PBM or their pharmacy assets.6

Conclusion: Strategic Recommendations for Policy Resiliency

The independent community pharmacy is a vital but endangered component of the American healthcare landscape. The evidence suggests that without significant regulatory intervention, the "last mile" of pharmaceutical care will continue to erode, particularly in the communities that need it most. To address these challenges, several policy pathways are recommended:

- Codifying Reimbursement Floors at the Federal Level: The success of Kentucky and West Virginia’s NADAC-plus-fee models demonstrates that cost-based reimbursement is both feasible and effective at stabilizing pharmacy networks.25

- Addressing the IRA Cash Flow Gap: CMS must implement a robust and rapid reimbursement mechanism for pharmacies dispensing MFP-negotiated drugs to prevent the forecasted $11,000 weekly cash flow shortfalls.28

- Mandatory Pass-Through Pricing: Eliminating spread pricing across all Medicaid and commercial plans would ensure that health dollars are used for patient care rather than PBM profit retention.11

- Strengthening Network Adequacy and Anti-Steering Laws: Regulatory frameworks should prohibit PBMs from using "preferred" status to steer patients toward affiliated pharmacies, ensuring that independent pharmacists can compete on a level playing field.1

- Recognizing Enhanced Clinical Services: Payers should provide standardized compensation for the value-added services—such as home delivery and adherence packaging—that independent pharmacies provide, recognizing their role in reducing overall healthcare expenditures through improved patient outcomes.13

The survival of the independent community pharmacy is not merely a matter of supporting small business; it is a critical imperative for maintaining a resilient and equitable public health infrastructure. As the primary advocates for patients in the complex world of modern medicine, these pharmacists provide the "heart behind the science" that no automated mail-order system can replace.19 Ensuring their viability is essential for the future of healthcare in America.

Works cited

- 2024 - FTC and Congress take action against PBMs for price gouging - ACAAI Member, accessed April 23, 2026, https://college.acaai.org/2024-ftc-and-congress-take-action-against-pbms-for-price-gouging/

- Federal Trade Commission's Interim Report Documents Harmful Impact of Pharmacy Benefit Managers on Independent Pharmacies - Duane Morris, accessed April 23, 2026, https://www.duanemorris.com/alerts/federal_trade_commissions_interim_report_documents_harmful_impact_pharmacy_benefit_0724.html

- The DIR Hangover One Year Later: How Have Pharmacists Fared ..., accessed April 23, 2026, https://www.drugtopics.com/view/the-dir-hangover-one-year-later-how-have-pharmacists-fared

- FTC Issues Interim Staff Report on Prescription Drug Middlemen: What Does It Mean and What Happens Next? | Advisories | Arnold & Porter, accessed April 23, 2026, https://www.arnoldporter.com/en/perspectives/advisories/2024/07/ftc-interim-staff-report-on-prescription-drug-middlemen

- FTC Launches Lawsuit Against PBMs - Freshfields, accessed April 23, 2026, https://www.freshfields.com/en/our-thinking/blogs/a-fresh-take/ftc-launches-lawsuit-against-pbms-102jk66

- Antitrust's Pharmaceutical Blind Spot — Cornell Undergraduate Law ..., accessed April 23, 2026, https://www.culsr.org/articles/antitrusts-pharmaceutical-blind-spot

- FTC Sues Pharmacy Benefit Managers Over “Artificially Inflated” Insulin Prices | Paul, Weiss, accessed April 23, 2026, https://www.paulweiss.com/insights/client-memos/ftc-sues-pharmacy-benefit-managers-over-artificially-inflated-insulin-prices

- FTC Releases Second Interim Staff Report on Prescription Drug ..., accessed April 23, 2026, https://www.ftc.gov/news-events/news/press-releases/2025/01/ftc-releases-second-interim-staff-report-prescription-drug-middlemen

- CMS Eliminates Retroactive DIR Fees - American Pharmacists Association, accessed April 23, 2026, https://www.pharmacist.com/Advocacy/Issues/CMS-Eliminates-Retroactive-DIR-Fees

- CMS Finalizes Changes to Pharmacy DIR in Part D Starting with Contract Year 2024, accessed April 23, 2026, https://www.ebglaw.com/insights/publications/cms-finalizes-changes-to-pharmacy-dir-in-part-d-starting-with-contract-year-2024

- KY SB50 - BillTrack50, accessed April 23, 2026, https://www.billtrack50.com/billdetail/1187314

- Q2 2024 State and Federal Regulatory and Legislative Activity Update - CarelonRx, accessed April 23, 2026, https://www.carelonrx.com/content/dam/digital/carelon/crx-assets/documents/2Q2024-federal-and-state-legislative-activity-report.pdf

- Patient Medication Adherence Among Pharmacies Participating in a North Carolina Enhanced Services Network - JMCP, accessed April 23, 2026, https://www.jmcp.org/doi/10.18553/jmcp.2020.26.6.718

- PHARMACY DESERTS AND ANTITRUST LAW - Boston University, accessed April 23, 2026, https://www.bu.edu/bulawreview/files/2024/12/LESLIE.pdf

- Pharmacy Closures and Medication Adherence P < .001 for all linear trends. - ResearchGate, accessed April 23, 2026, https://www.researchgate.net/figure/Pharmacy-Closures-and-Medication-Adherence-P-001-for-all-linear-trends_fig2_332537559

- Community Pharmacy Enhanced Services Network (CPESN), accessed April 23, 2026, https://www.communitycarenc.org/population-management/pharmacy/community-pharmacy-enhanced-services-network-cpesn

- Harbor House of Louisville | GoToLouisville.com Official Travel Source, accessed April 23, 2026, https://www.gotolouisville.com/directory/harbor-house-of-louisville/

- Programs & Services - Harbor House, accessed April 23, 2026, https://hhlou.org/programs-services/

- KENTUCKY PHARMACY – Text 502-694-2441 – Kentucky ..., accessed April 23, 2026, https://kypharmacy.net/

- Pharmacy - Home of the Innocents, accessed April 23, 2026, https://homeoftheinnocents.org/service-programs/pharmacy/

- Rutledge v. Pharmaceutical Care Management Association - Oyez, accessed April 23, 2026, https://www.oyez.org/cases/2020/18-540

- Supreme Court Holds Arkansas Statute Regulating PBMs Not Preempted By ERISA, accessed April 23, 2026, https://www.afslaw.com/perspectives/health-care-counsel-blog/supreme-court-holds-arkansas-statute-regulating-pbms-not

- KY SB50 | 2020 | Regular Session - LegiScan, accessed April 23, 2026, https://legiscan.com/KY/bill/SB50/2020

- Single Pharmacy Benefit Manager, accessed April 23, 2026, https://ncpa.org/sites/default/files/2023-11/KY_Single_PBM_PPT_Oct_23.pdf

- EPIC Rx Legislative Wins: First Quarter of 2024, accessed April 23, 2026, https://www.epicrx.com/epic-rx-legislative-wins-first-quarter-of-2024/

- SUPPORT SENATE BILL 188! Expand the Benefits of PBM Reform to Kentucky Industry and Businesses Pharmacy benefit managers (PBMs), accessed April 23, 2026, https://kam.us.com/wp-content/uploads/2024/03/KAM-KRF-Joint-Statement-Supporting-SB-188.pdf

- WEST VIRGINIA LEGISLATURE Senate Bill 453, accessed April 23, 2026, https://www.wvlegislature.gov/Bill_Text_HTML/2024_SESSIONS/RS/bills/sb453%20sub1.pdf

- New Analysis Finds the Medicare Drug Price Negotiation Program Threatens Financial Stability of American Pharmacies - The National Community Pharmacists Association | NCPA, accessed April 23, 2026, https://ncpa.org/newsroom/news-releases/2025/01/30/new-analysis-finds-medicare-drug-price-negotiation-program

- Operational and Policy Considerations in the Effectuation of Medicare's Maximum Fair Drug Prices for Part D - USC Schaeffer, accessed April 23, 2026, https://schaeffer.usc.edu/research/medicare-drug-prices-mfp-effectuation/

- How the Inflation Reduction Act has improved Medicare prescription drug coverage, accessed April 23, 2026, https://www.medicareresources.org/blog/how-the-inflation-reduction-act-has-improved-medicare-part-d-prescription-drug-coverage/

- March 2025 report to the Congress--Chapter 12: The Medicare prescription drug program (Part D) - MedPAC, accessed April 23, 2026, https://www.medpac.gov/wp-content/uploads/2025/03/Mar25_Ch12_MedPAC_Report_To_Congress_SEC.pdf

- Recent Developments in Antitrust Litigation 2025 - American Bar Association, accessed April 23, 2026, https://www.americanbar.org/groups/business_law/resources/business-law-today/2025-august/recent-developments-antitrust-litigation/

- IN RE: TECFIDERA ANTITRUST LITIGATION | 1:2024cv07387 | N.D. Ill. - CaseMine, accessed April 23, 2026, https://www.casemine.com/judgement/us/697c4d8f8d0afcd812681173

- Executive Summary Status of Adoption – HL7®/NCPDP Pharmacist eCare Plan, accessed April 23, 2026, https://www.ncpdp.org/NCPDP/media/pdf/ExecutiveSummary_PeCP.pdf